.svg)

In today's digital age, accepting payments is the lifeblood of any online business. But behind the seemingly simple act of a customer clicking "pay," lies a complex ecosystem.

Understanding the intricacies of payment processing is crucial for any businesses to optimize revenue, minimize costs, and ensure a seamless customer experience. This guide aims to explain the ecosystem of payments, providing merchants with a foundational understanding of its complexities, and why one Payment Service Provider ('PSP') may be very different from another PSP when it comes to underlying infrastructure.

The Players in the Payment Ecosystem

To start, we need to understand the key parts of the card ecosystem, the various players, what role they all play, and who is responsible for what part:

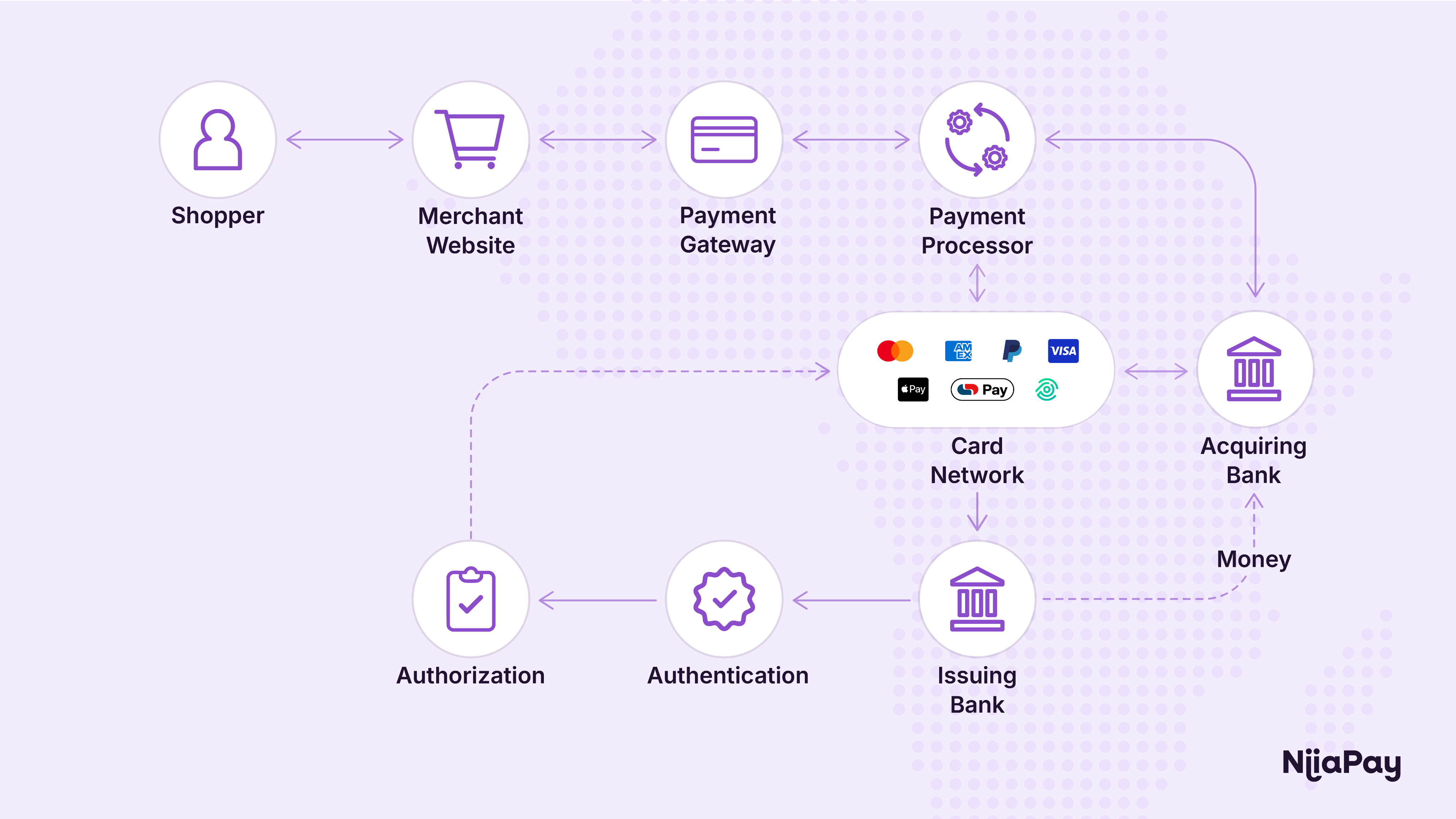

- Payment Gateways: Technical providers who securely accept and transmit sensitive transactional data from the merchant website

- Payment Processors: Companies that handle the technical ('ISO') message aspects of processing card payments between the banks and networks

- Issuing Banks: Banks that issue credit or debit cards to customers, and hold the relationship with the cardholder

- Acquiring Banks: Banks that receive the funds on behalf of merchants, and bear the financial risk. An acquiring bank can also be an issuing bank, but it is not always the case

- Card Networks (Visa, Mastercard, etc.): Organizations that facilitate communication between issuing and acquiring banks (via processors)

The Transaction Journey

While some of these players are often used interchangeably (i.e. Processor & Acquiring Bank), and referred to as PSPs, there are usually distinct entities involved, especially in emerging markets.

Step-by-Step Transaction Flow:

- Shopper: The process begins with the customer initiating a purchase

- Merchant Website: The shopper enters their payment details on the merchant's platform

- Payment Gateway: The gateway securely collects the card and merchant information

- Payment Processor: The gateway sends this data to the payment processor, who formats it into a standardized message (ISO8583)

- Card Network (Amex, Visa, Mastercard): The processor routes the formatted message to the appropriate card network

- Issuing Bank: The network forwards the authorization request to the shopper's bank (the issuer)

- Verification: The issuing bank verifies the shopper's funds and the validity of the card

- Authorization Response: The issuing bank sends an approval or decline response back through the network and the processor to the gateway

- Authorization Result: The gateway informs the merchant and the shopper about the transaction status

Sub-process (Transaction Approved):

- Funds Cleared: The funds are debited from the shopper's account

- Issuer: The funds are held by the issuing bank

- Acquiring Bank: The issuer then transfers the funds to the merchant's bank (the acquiring bank)

- Merchant Account: Finally, the acquiring bank deposits the funds into the merchant's bank account

Impact on Merchant Business

As shown above, there are multiple parties involved in a payment, and it only takes one part of the ecosystem to have an issue for the flow of a transaction to be impacted.

In more mature markets, some newer payments companies like Adyen, Checkout.com, and Stripe have taken more control of the payments flow by building each part themselves. But unfortunately, the truth is that in most emerging markets (i.e. Nigeria & South Africa), the ecosystems are still fragmented.

However, there are ways for businesses to minimize their risk while also optimize payments, so they can reduce their cost and increase their revenue.

Key Optimization Strategies:

Redundancy (adding a second PSP) is the best way to reduce the risk when one PSP has issues. It does not only mitigate the risk of one PSP having outages, but a second PSP also allows for smart routing and retries on "soft declines". This can help recuperate some of the refused transactions, due to technical errors in one of the value chains.

Having two different Acquiring Banks might also influence payments, since "on-us" transactions - same Issuer and Acquiring Bank (i.e. Absa Debit card on Absa Acquiring) - can generate higher authorization rates.

In addition, if you get the same refusal reason on both attempts (i.e. "Transaction not permitted"), you can block the user from trying the same card a second time, and advise them to try another card/method, trying to convert the user at the point of paying.

Advice for Navigating the Complexities

The first thing a merchant should do is to understand their customer base, and what payment methods they use most frequently. This may also influence which PSP you decide to work with. Secondly, they need to conduct a detailed analysis and see what the performance of the PSP(s) is.

A merchant should look at data points such as:

- What is the success (auth) rate with my current PSP?

- What are the refusal reasons?

- What is the conversion rate for each of my payment methods?

- How many refused payments can be attempted to recuperate?

- How many "hard declines" occurred?

- What costs were preventable?

This will help merchants make informed decisions, as to which of the several areas in navigating the payment landscape to focus on.

Optimizing Your Payment Strategy

To succeed in the complex world of payments, merchants should ensure they understand the following:

- Their Customer Base: Identify the preferred payment methods of their target audience. (BNPL for 25-45 year old women, vs Card for 55-65 year old men)

- Compare Payment Providers: Analyze and compare different payment gateways and processors to find the best performing one for your industry and business

- Monitor Transaction Fees: Regularly review and optimize transaction fees to minimize costs

- Streamline Fraud Management: Develop effective strategies for preventing and managing fraud

- Embrace Technology: Leverage technology solutions to automate payment processes and improve efficiency

Payment Terms Glossary

Merchant ID: A specialized bank account that allows merchants to accept credit and debit card payments.

Chargebacks: Disputes initiated by customers with their issuing banks, resulting in funds being reversed from the merchant's account.

PCI DSS Compliance: A set of security standards designed to protect cardholder data.

Transaction Fees: Costs associated with processing payments, including interchange fees, assessment fees, and processor fees.

Acquiring Fee: Also referred to as Merchant Discount Rate (MDR).

Payment Methods: The various ways customers can pay, including credit/debit cards, digital wallets, mobile payments, and bank transfers.

Key Areas to Focus On

- Choosing the Right Payment Providers: Selecting payment gateways and processors that align with their business needs and target audience

- Managing Transaction Fees: Understanding and optimizing transaction fees to minimize costs

- Ensuring Security and Compliance: Implementing robust security measures to protect sensitive data and comply with regulations

- Handling Chargebacks: Developing effective strategies for preventing and managing chargebacks

- Integrating Payment Systems: Seamlessly integrating payment systems with existing business software

- International Payments: Handling cross-border transactions and currency conversions

Conclusion

The payment landscape is constantly evolving, and merchants must stay informed and adapt to remain competitive. By understanding the complexities of payment processing and implementing effective strategies, merchants can optimize their payment operations, enhance the customer experience, and drive business growth.

Remember that authentication (3DS), when used intelligently, cannot only help protect your business from fraud, but it can also help increase authorization rates. The key is to approach payments strategically, with a deep understanding of your customer base and the technical infrastructure supporting your transactions.